-1.png?height=120&name=SAPP%20logo%20m%E1%BB%9Bi-01%20(1)-1.png)

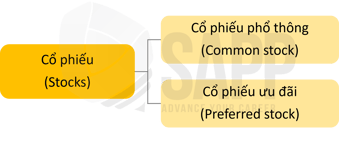

Có hai loại cổ phiếu doanh nghiệp là cổ phiếu phổ thông và cổ phiếu ưu đãi. Cổ phiếu phổ thông là vốn được huy động của công ty. Trong khi cổ phiếu ưu đãi là sự kết hợp giữa nợ và vốn chủ sở hữu.

1. Cổ phiếu phổ thông (Common stock)

b. Các quyền lợi khi sở hữu cổ phiếu phổ thông

2. Cổ phiếu ưu đãi (Preferred stock)

I. Mục tiêu

- Tìm hiểu về cổ phiếu phổ thông và cổ phiếu ưu đãi.

- Xác định ưu điểm và nhược điểm của cổ phiếu phổ thông và cổ phiếu ưu đãi.

II. Nội dung

Trong bài học này chúng ta sẽ tìm hiểu về:

- Các loại cổ phiếu và đặc điểm của chúng.

- Quyền lợi khi sở hữu các loại cổ phiếu.

1. Cổ phiếu phổ thông (Common stock)

a. Định nghĩa

Cổ phiếu phổ thông là một hình thức huy động vốn có lợi cho doanh nghiệp. Nó được báo cáo trong phần vốn chủ sở hữu của cổ đông trên bảng cân đối kế toán của công ty.

b. Các quyền lợi khi sở hữu cổ phiếu phổ thông

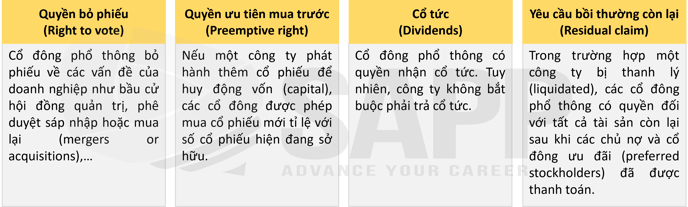

Quyền sở hữu cổ phần (Ownership shares) trong một công ty được gọi là vốn chủ sở hữu (equity) hoặc cổ phiếu (stock). Cổ phiếu phổ thông là loại cổ phiếu quan trọng nhất.

Cổ đông phổ thông (Common stockholders) có các quyền sở hữu (ownership rights) bao gồm:

c. Thị trường cung cấp

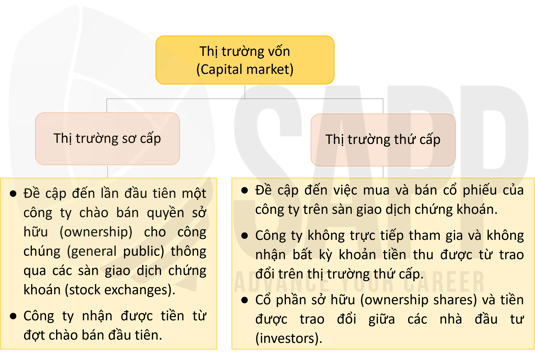

Cổ phiếu phổ thông có thể được mua trên thị trường vốn (Capital market) bao gồm thị trường vốn sơ cấp (primary) và thứ cấp (secondary).

d. Đánh giá

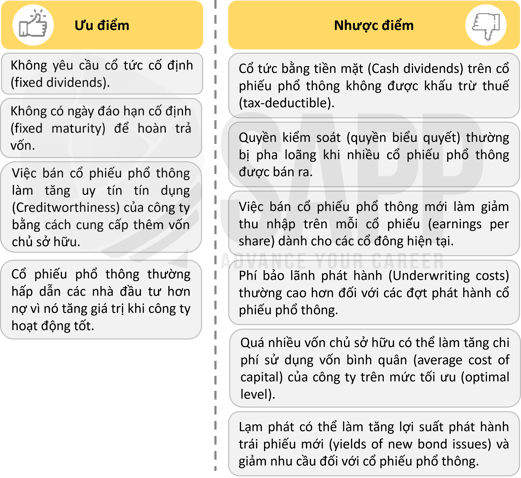

Cổ phiếu phổ thông có một số ưu điểm và nhược điểm đối với tổ chức phát hành như sau:

2. Cổ phiếu ưu đãi (Preferred stock)

a. Định nghĩa

Cổ phiếu ưu đãi (Preferred stock) là sự kết hợp giữa nợ (debt) và vốn chủ sở hữu (equity). Cổ phiếu ưu đãi có một khoản phí cố định và tăng đòn bẩy (leverage), nhưng việc thanh toán cổ tức không phải là nghĩa vụ pháp lý.

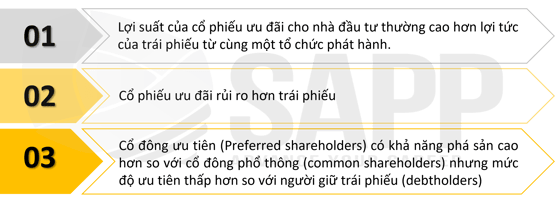

b. Đặc điểm

Cổ phiếu ưu đãi có những đặc điểm sau:

c. Điều khoản khi phát hành cổ phiếu ưu đãi

Các điều khoản phổ biến (Typical provisions) khi phát hành cổ phiếu ưu đãi được trình bày như sau:

|

Quyền ưu tiên về tài sản và thu nhập (Priority in assets and earnings) |

Nếu công ty phá sản, các cổ đông ưu tiên được ưu tiên hơn so với các cổ đông phổ thông. |

|

Cổ tức tích lũy (Accumulation of dividends) |

Nếu cổ tức ưu đãi (preferred dividends) được tích lũy, cổ tức còn thiếu (dividends in arrears) phải được thanh toán trước khi cổ tức thông thường (common dividends) được thanh toán. |

|

Quyền tham gia chia lãi (Participation) |

Cổ phiếu ưu đãi có thể tham gia vào thu nhập vượt mức (excess earnings) của công ty. Ví dụ: cổ phiếu ưu đãi dự phần (participating preferred stock) ở mức 8% có thể trả cổ tức mỗi năm lớn hơn mức 8% khi công ty thu được nhiều lợi nhuận, nhưng cổ phiếu ưu đãi không tham gia chia lãi (nonparticipating preferred stock) sẽ không nhận được nhiều hơn số tiền được ghi trên mặt cổ phiếu. |

|

Mệnh giá (Par value) |

Mệnh giá là giá trị thanh lý (liquidation value) và tỷ lệ phần trăm của mệnh giá bằng với cổ tức ưu đãi. |

|

Quyền hoàn lại (Redeemability) |

Một số cổ phiếu ưu đãi có thể được hoàn lại tại một thời điểm nhất định hoặc theo lựa chọn của người nắm giữ. |

|

Quyền biểu quyết (Voting rights) |

Người nắm giữ cổ phiếu ưu đãi thường không được cấp quyền biểu quyết. |

|

Quyền rút lại (Retirement) |

· Cổ phiếu ưu đãi có thể chuyển đổi thành cổ phiếu phổ thông theo lựa chọn của cổ đông. · Tổ chức phát hành có thể mua lại cổ phiếu. Ví dụ: cổ phiếu có thể không thể thu hồi trong một khoảng thời gian nhất định, sau đó nó có thể được thu hồi nếu người phát hành trả phí tiền mua quyền chuộc lại cổ phiếu – call premium (số tiền vượt trên mệnh giá). · Cổ phiếu ưu đãi có thể có quỹ thanh toán nợ (sinking fund) cho phép mua một tỷ lệ phần trăm nhất định hàng năm của số cổ phiếu đang lưu hành. |

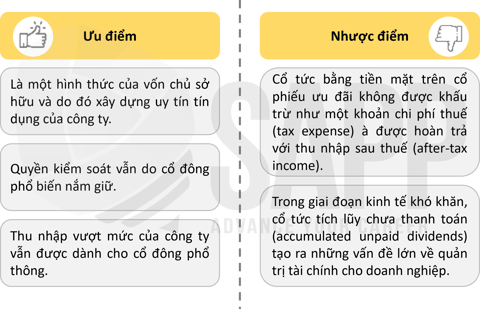

d. Đánh giá

Cổ phiếu ưu đãi có một số ưu điểm và nhược điểm đối với tổ chức phát hành như sau:

III. Bài tập

Question 1:

The par value of a common stock represents:

| A. | The liability ceiling of each original shareholder when a company undergoes bankruptcy proceedings if the original shareholder purchased the common stock for a price less than par value. |

| B. | The total value of the stock that must be entered in the issuing corporation's records. |

| C. | A theoretical value of $100 per share of stock with any differences entered in the issuing corporation's records as discount or premium on common stock. |

| D. | The amount that must be recorded on the issuing corporation's record as paid-in capital. |

Answer:

The correct answer is choice A.

A is correct. Par value (or legal capital) is the amount of capital that must be retained by the corporation for the protection of its creditors and cannot be paid out as dividends. The amount received by a company from the sale of its capital stock (common and preferred) is reported in shareholders' equity. Par value is usually a nominal amount and is not related to market value. The par value or legal capital represents a limit on each original shareholder's liability if the original shareholder purchased the common stock for a price less than par value. The par value of a common stock represents the liability ceiling of each original shareholder either when a company undergoes bankruptcy proceedings if the original shareholder purchased the common stock for a price less than par value or the company dissolves, company debts remain unpaid, and the original shareholder purchased the common stock for a price less than par value.

B is incorrect. The par value of a common stock does not represent the total value of the stock that must be entered in the issuing corporations' records. The total value entered in the corporation's records is the par value and paid-in capital, if any, in excess of par value.

C is incorrect. Minimum value of par is not arbitrarily set at $100 per share. Minimum par values may be set by state law but are usually nominal amounts less than $1 per share.

D is incorrect. Par value of a common stock is not the amount that must be recorded as paid-in- capital. Amounts received from the sale of common stock are usually in excess of the stock's par value. The purchase price includes both par value and paid-in capital, if any, in excess of par value.

Question 2:

The participating feature for a preferred stock means that preferred stockholders have the opportunity to:

| A. | Sell all or part of the shares back to the issuer at a pre-specified call price. |

| B. | Increase their dividends when common stockholders' dividends reach a certain amount. |

| C. | Convert preferred stock into a specified amount of common stock. |

| D. | Be granted special voting privileges if the corporation is unable to pay the fixed dividend. |

Answer:

The correct answer is choice B.

B is correct. By definition, a participating feature allows preferred stockholders to participate in increasing dividends when common stockholders' dividends reach a certain amount. The exact amount of participation varies and is determined by some predetermined formula that relates additional preferred stockholder payouts to increases in common stockholder payouts.

A is incorrect. The participating feature for a preferred stock does not mean that preferred stockholders have the opportunity to sell all or part of the shares back to the issuer at a pre-specified call price.

C is incorrect. The participating feature for a preferred stock does not mean that preferred stockholders have the opportunity to convert preferred stock into a specified amount of common stock.

D is incorrect. The participating feature for a preferred stock does not mean that preferred stockholders have the opportunity to be granted special voting privileges if the corporation is unable to pay the fixed dividend.