Phương pháp tính giá theo quy trình được sử dụng khi quá trình sản xuất sản phẩm của doanh nghiệp cần trải qua quá nhiều công đoạn, ví dụ như: sản xuất hóa chất, chế biến thức ăn đóng hộp. Một lưu ý phải kể đến đó là, tổng khối lượng của sản phẩm đầu vào sẽ không nhất thiết phải bằng với khối lượng của sản phẩm đầu ra do tồn tại hao hụt trong quá trình sản xuất.

1. Cơ sở của Process costing

Phương pháp giá thành theo quy trình là một phương pháp tính giá thành để xác định chi phí của sản phẩm tại mỗi quy trình hoặc giai đoạn sản xuất. Chi phí được tính trung bình trên các đơn vị được sản xuất trong kỳ. Chi phí quá trình phù hợp cho các ngành sản xuất các sản phẩm đồng nhất và trong đó sản xuất là một dòng chảy liên tục.

Các sản phẩm cần trải qua nhiều công đoạn sản xuất liên tục như:

- Lọc dầu

- Giấy

- Thức ăn và đồ uống

- Hoá chất

- Lon và hộp thiếc (khối lượng lớn, chi phí thấp)

2. Các đặc trưng

- Đầu ra của khâu này là đầu vào của khâu tiếp theo, liên tục cho tới khi sản phẩm hoàn thành.

- Không thể phân tách chi tiết từng phần chi phí kết tinh trong cost per unit of output/ closing inventory.

- Thường xảy ra hao hụt, tiêu hao trong quá trình sản xuất do hỏng hóc, lãng phí, bốc hơi,… (spoilage, wastage, evaporation).

- Sản phẩm của cả quá trình sản xuất có thể bao gồm chính phẩm, sản phẩm phụ, sản phẩm liên kết (single products, by-product, joint products).

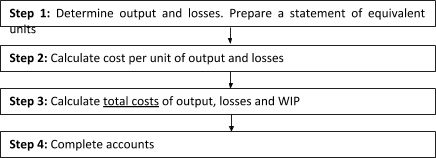

3. Các bước tiến hành process costing

|

Các bước |

Chi tiết |

|

Bước 1: Xác định sản lượng và tiêu hao |

- Xác định sản lượng dự kiến - Xác định chi phí tiêu hao thông thường và chi phí tiêu hao bất thường - Xác định đơn vị sản lượng tương đương (nếu có giá trị HTK đầu kì và cuối kì) |

|

Bước 2: Xác định chi phí trên từng đơn vị của tổng sản lượng, hao hụt và các sản phẩm dở dang (WIP) |

- Xác định chi phí trên từng đơn vị sản phẩm tương đương |

|

Bước 3: Tính tổng chi phí đầu ra và thất thoát tổng sản lượng, hao hụt và các sản phẩm dở dang (WIP) |

- Tính tổng chi phí đầu ra - Tổng chi phí tiêu hao thông thường - Tổng chi phí tiêu hao bất thường |

|

Bước 4: Tài khoản hoàn thiện |

- Hoàn thiện tài khoản process và xóa bỏ những khoản tương ứng |

4. Tiêu hao trong process costing

Trong quá trình sản xuất luôn luôn xảy ra tiêu hao. Nếu một mức độ thiệt hại như kỳ vọng, điều này được gọi là tiêu hao thông thường. Nếu tiêu hao lớn hơn dự kiến, phần mất thêm là tiêu hao bất thường. Nếu tiêu hao ít hơn dự kiến, phần chênh lệch được gọi là lợi ích bất bình thường.

Sản phẩm tiêu hao hoặc hư hỏng có thể có giá trị thanh lý.

a. Các mức độ tiêu hao

|

Normal loss: expected loss |

Abnormal loss: actual loss > expected loss |

Abnormal gain: actual loss < expected loss |

|

Là một loại chi phí (cost) |

Là một loại chi phí (cost) |

Là một chi phí âm (negative cost) |

|

Cost per unit = Normal loss incurred per unit |

Cost per unit = |

|

|

Cách ghi nhận chi phí tiêu hao phát sinh:

|

||

b. Ví dụ minh họa

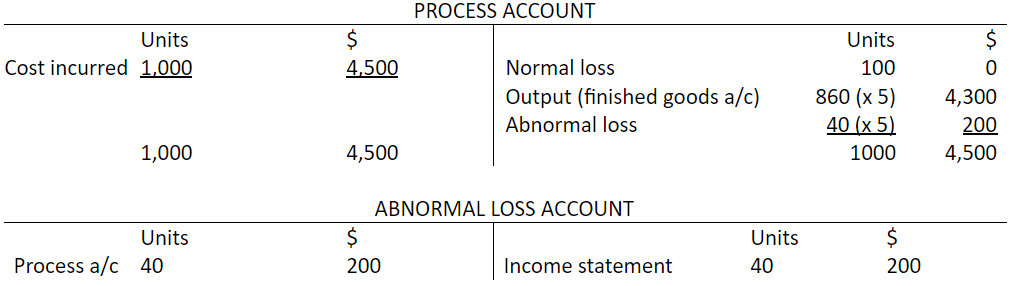

Suppose that input to a process is 1,000 units at a cost of $4,500. Normal loss is 10% and there are no openings or closing stocks. Determine the accounting entries for the cost of output and the cost of the loss if actual output were as follows.

(a) 860 units (so that actual loss is 140 units)

(b) 920 units (so that actual loss is 80 units)

Answer:

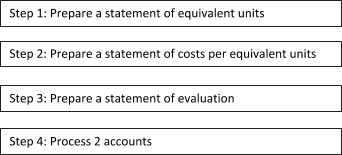

(a) Output is 860 units – 4 steps:

Step 1: Determine output and losses

Nếu Actual output là 860 units và Actual loss là 140 units:

|

Actual loss |

140 |

|

Normal loss (10% of 1,000) |

100 |

|

Abnormal loss |

40 |

Step 2: Calculate cost per unit of output and losses

Cost per unit of output và Cost per unit of abnormal loss dựa trên Expected output:

Step 3: Calculate total cost of output and losses (Normal loss không được ghi nhận là chi phí)

|

Units |

|

|

Cost of output (860 x $5) |

4,300 |

|

Normal loss (of 1,000) |

0 |

|

Abnormal loss (40 x $5) |

200 |

|

4,500 |

Step 4: Complete accounts

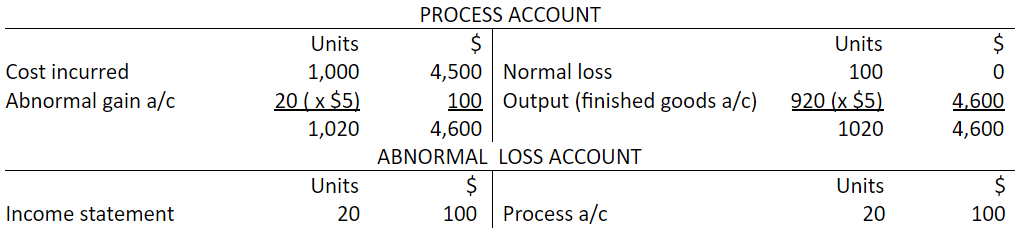

(b) Output is 920 units

Step 1: Determine output

Nếu Actual output là 920 units và Actual loss là 80 units.

|

Units |

|

|

Actual loss |

80 |

|

Normal loss (10% of 1,000) |

100 |

|

Abnormal loss |

20 |

Step 2: Calculate cost per unit of output and losses

Cost per unit of output và Cost per unit of abnormal gain đều dựa trên Expected output.

(Dù là Abnormal loss hay Abnormal gain thì cũng không ảnh hưởng tới giá trị sản phẩm đầu ra. Phần chi phí đơn vị sản phẩm ở 2 phần là giống nhau.)

Step 3: Calculate total cost of output and losses

|

$ |

|

|

Cost of output (920 x $5) |

4,600 |

|

Normal loss |

0 |

|

Abnormal gain (20 x $50) |

(100) |

|

4,500 |

Step 4: Complete accounts

5. Tiêu hao và giá trị thu hồi (scrap value/ salvage value/ residual value)

Với normal loss: Scrap value thường được trừ vào chi phí NVL cost of materials.

Với abnormal loss: Scrap value của abnormal loss (hay abnormal gain) thường được set off against (bù trừ) với chi phí chính nó đã phát sinh trên tài khoản Abnormal gain/loss.

a. 3 bước để ghi nhận giá trị thu hồi:

Bước 1: Tách riêng Scrap value của Normal loss với Scrap value của Abnormal gain/loss.

Bước 2: Trừ Scrap value của Normal loss khỏi Cost of process: Cr Process cost a/c.

Bước 3: Trừ Scrap value của Abnormal loss/gain: Cr Abnormal loss a/c hoặc Dr Abnormal gain a/c.

Ghi nhận cash received từ scrap: Dr Cash và Cr Scrap a/c.

b. Ví dụ minh họa

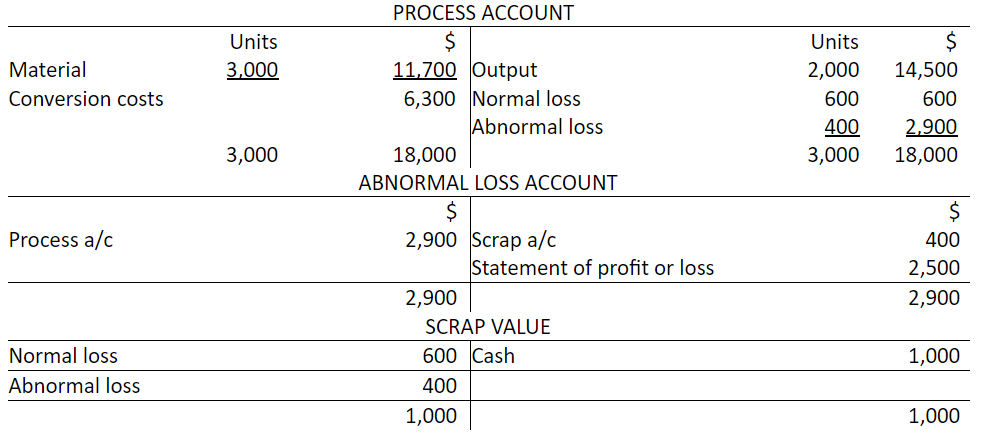

3,000 units of material are input to a process. Process costs are as follows.

|

Material |

$11,700 |

|

Conversion costs |

$6,300 |

|

Output is |

2,000 units. |

|

Normal loss is |

20% of input. |

|

The units of loss could be sold for |

$1 each. |

|

Required: Prepare appropriate accounts. |

|

|

Answer: Step 1: Determine output and losses |

|

|

Units |

|

|

Input |

3,000 |

|

Normal loss (20% of 3,000) |

600 |

|

Expected output |

2,400 |

|

Actual output |

2,000 |

|

Abnormal loss |

400 |

|

Step 2: Calculate cost per unit of output and losses |

$ |

|

Scrap value of normal loss |

600 |

|

Scrap value of abnormal loss |

400 |

|

Total scrap (1,000 units x $1) |

1,000 |

|

Cost expected unit = [(11,700 – 600) + 6,300] / 2,400 = $7.25 |

|

|

Step 3: Calculate total cost of output and losses |

$ |

|

Output (2,000 x $7.25) |

14,500 |

|

Normal loss (600 x $1.00) |

600 |

|

Abnormal loss (400 x $7.25) |

2,900 |

|

18,000 |

Step 4: Complete accounts

6. Tiêu hao và chi phí thanh lý

a. Cơ sở ghi nhận

Tùy từng trường hợp mà đề bài cung cấp dữ liệu và yêu cầu, ta xác định như sau:

- Disposal cost của Normal loss unit sẽ làm tăng Process cost, khiến cost per unit thay đổi, dẫn tới giá trị sản phẩm đầu ra (output value) và abnormal loss/gain cũng biến động theo.

- Normal loss vẫn không được ghi nhận vào Process cost.

- Disposal cost của Normal loss: Dr Process a/c.

- Disposal cost của Abnormal loss ghi nhận vào Abnormal loss a/c => ảnh hưởng tới SOPL.

b. Ví dụ minh họa

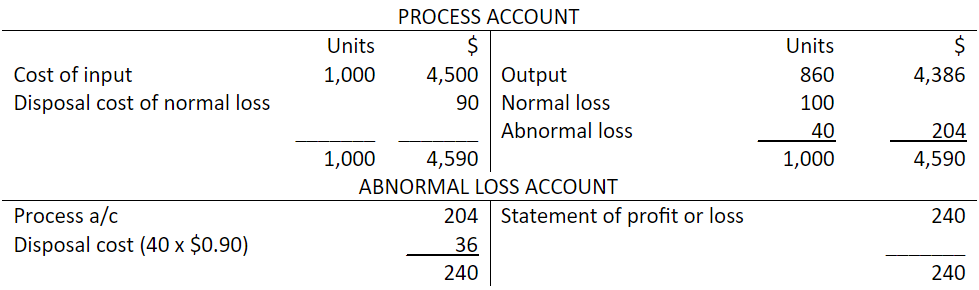

Suppose that input to a process was 1,000 units at a cost of $4,500. Normal loss is 10% and there are no opening and closing inventories. Actual output was 860 units and loss units had to be disposed of at a cost of $0.90 per unit.

Normal loss = 10% x 1,000 = 100 units.

Abnormal loss = 900 – 860 = 40 units

Cost per unit = [4,500 + (100 x $0.90)]/900 = $5,100

The relevant accounts would be as follows:

7. Xác định giá trị sản phẩm dở dang đầu kì và cuối kì (opening & closing WIP)

Để xác định giá trị sản phẩm hoàn thành trong kì, trước hết chúng ta phải xác định giá trị sản phẩm dở dang đầu kì và cuối kì, quy đổi chúng ra giá trị sản phẩm hoàn thành tương đương (VD như 2 sản phẩm dở dang mới hoàn thành 50% tương đương với 1 sản phẩm hoàn thành 100%).

a. 4 bước xác định giá trị SPDD cuối kì

b. Xác định giá trị SPDD đầu kì: 2 phương pháp: FIFO và Weighted Average Cost

FIFO method:

i) Giả định: Tất cả SPDD đầu kì đều sẽ được hoàn thành đầu tiên trong kì.VD như đầu kì có 200 SPDD mới hoàn thành 50% và trong kì đưa vào sản xuất thêm 1000 sản phẩm mới, cuối kì còn 300 SPDD. Ta phân tích:

- Đầu kì: 200 SPDD 50%

- Trong kì:

- Sản phẩm mới đưa vào sản xuất: 1000 sản phẩm.

- Số sản phẩm hoàn thành trong kì: 200 + 1000 – 300 = 900 SPHT, trong đó:

- 200 SPHT là SPDD đầu kì được hoàn thiện.

- 900 – 200 = 700 SPHT là sản phẩm mới đưa vào sản xuất và hoàn thành trong kì.

-

-

- Cuối kì: còn 300 SPDD: đều là sản phẩm mới đưa vào sản xuất trong kì nhưng chưa hoàn thành, không bao gồm SPDD đầu kì.

ii) Các bước xác định giá trị SPDD:

iii) Ví dụ minh họa:

Suppose that information relating to process 1 of a 2-stage production process is as follows, for August 20X2.

|

Opening inventory 500 units: degree of completion |

60% |

|

Cost to date |

$2,800 |

|

Cost incurred in August 20X2 |

$ |

|

Direct materials (2,500 units introduced) |

13,200 |

|

Direct labor |

6,600 |

|

Production overhead |

6,600 |

|

26,400 |

|

|

Closing inventory 300 units: degree of completion |

80% |

|

There was no loss in the process. |

Required:

Prepare the process 1 account for August 20X2.

Answer:

Do áp dụng phương pháp FIFO nên ở đây có thể dễ dàng xác định rằng trong tháng 8/20X2 thì những SPHT được hoàn thành đầu tiên là Opening inventory.

Mỗi sản phẩm của opening inventories:

Đã hoàn thành = 60%

Trong tháng 8/X2 cần hoàn thiện thêm = 40%

Chi phí đã phát sinh tính tới 1/8/20X2 là $2,800, suy ra chi phí của SPHT sẽ là $2,800 cộng với chi phí phát sinh để hoàn thành nốt 40% còn lại.

Sau khi tất cả SPDD đầu kì được hoàn thành trở thành SPHT thì những sản phẩm được đưa vào sản xuất trong kì sẽ được tiến hành sản xuất và hoàn thành.

|

|

Units |

|

Tổng SPHT trong tháng 8 (500 + 2,500 – 300) |

2,700 |

|

SPDD đầu kì được hoàn thành trong kì |

500 |

|

SP mới đưa vào sản xuất và hoàn thành trong kì |

2,200 |

Như ta đã phân tích, trong 2,700 SPHT trong tháng 8 thì có:

- 500 SPHT là SPDD đầu kì được hoàn thiện trong kì.

- 2,200 SPHT là SP mới đưa vào sản xuất và hoàn thành trong kì.

Ngoài ra, có 300 SP được đưa vào sản xuất trong kì song chưa được hoàn thiện, trở thành SPDD cuối kì.

The total cost of output to process 2 during 20X2 will be as follows.

|

|

$ |

|

Opening inventory: cost brought forward |

2,800 (60%) |

|

plus cost incurred during August 20X2, |

|

|

to complete |

x (40%) |

|

|

2,800 + x |

|

Fully worked 2,200 units |

y |

|

Total cost of output to process 2, FIFO basis |

2,800 + x + y |

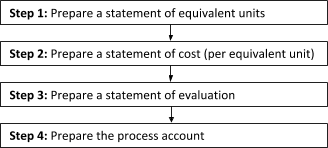

Step 1: Determine output and losses

STATEMENT OF EQUIVALENT UNITS

|

Total units |

% |

Equivalent of production in Aug 20X2 |

|

|

Opening inventory units completed |

500 |

40 |

200 |

|

Fully worked units |

2,200 |

100 |

2,200 |

|

Output to process 2 |

2,700 |

2,400 |

|

|

Closing inventory |

300 |

80 |

240 |

|

3,000 |

2,640 |

Step 2: Calculate cost per unit of output and losses

The cost per equivalent unit in August 20X2 can now be calculated.

STATEMENT OF COST PER EQUIVALENT UNIT

|

Cost incurred |

$26,400 |

|

Equivalent units |

2,640 |

|

Cost per equivalent unit |

$10 |

Step 3: Calculate total costs of output, losses and WIP

STATEMENT OF EVALUATION

|

Equivalent units |

Valuation |

|

|

$ |

||

|

Opening inventory, work done in August 20X2 |

200 |

2,000 |

|

Fully worked units |

2,200 |

22,000 |

|

Closing inventory |

240 |

2,400 |

|

2,640 |

26,400 |

The total value of the completed opening inventory will be $2,800 (brought forward) plus $2,000 added in August before completion = $4,800.

Step 4: Complete accounts

PROCESS 1 ACCOUNT

|

Units |

$ |

Output to process 2: |

Units |

$ |

|

|

Opening inventory |

500 |

2,800 |

Opening inventory |

500 |

4,800 |

|

Direct materials |

2,500 |

13,200 |

Fully worked units |

2,200 |

22,000 |

|

Direct labor |

6,600 |

2,700 |

26,800 |

||

|

Production overheads |

6,600 |

Closing inventory |

300 |

2,400 |

|

|

3,000 |

29,200 |

3,000 |

29,200 |

We now know that the value of x is $(4,800 – 2,800) = $2,000 and the value of y is $22,000.

Weighted Average Cost method: 4 bước

Ở phương pháp này, chúng ta không phân biệt giữa SPDD đầu kì và SP mới đưa vào sản xuất trong kì như trong FIFO, mà tính chi phí bình quân tương đương cho chúng (weighted average cost).

Ví dụ minh họa:

Magpie produces an item which is manufactured in two consecutive processes. Information relating to process 2 during September 20X3 is as follows.

Opening inventory 800 units

Degree of completion:

|

$ |

||

|

Process 1 materials |

100% |

4,700 |

|

Added materials |

40% |

600 |

|

Conversion costs |

30% |

1,000 |

|

6,300 |

During September 20X3, 3,000 units were transferred from process 1 at a valuation of $18,100. Added materials cost $9,600 and conversion costs were $11,800.

Closing inventory at 30 September 20X3 amounted to 1,000 units which were 100% complete with respect to process 1 materials and 60% complete with respect to added materials. Conversion costs work was 40% complete.

Magpie used a weight average cost system for valuation of output and closing inventory.

Required: Prepare the process 2 account for September 20X3.

Answer:

Step 1: Opening inventory units count as a full equivalent unit of production when the weighted average cost system is applied. Closing inventory equivalent units are assessed in the usual way.

STATEMENT OF EQUIVALENT UNITS

|

Equivalent units |

Total units |

% |

Process material |

% |

Added material |

% |

Conversion costs |

|

Closing inventory |

800 |

100 |

800 |

800 |

800 |

||

|

Fully worked units * |

2,000 |

100 |

2,000 |

2,000 |

2,000 |

||

|

Output to finished goods |

2,800 |

2,800 |

2,800 |

2,800 |

|||

|

Closing inventory |

1,000 |

100 |

1,000 |

60 |

600 |

40 |

400 |

|

3,800 |

3,800 |

3,400 |

3,200 |

* 3,000 units from process 1 minus closing inventory of 1,000 units

Step 2: The cost of opening inventory is added to costs incurred in September 20X3, and a cost per equivalent unit is then calculated.

STATEMENT OF COSTS PER EQUIVALENT UNIT

Step 3: Statement of evaluation

Step 4: Process 2 accounts

PROCESS 2 ACCOUNT

|

Units |

$ |

Units |

$ |

||

|

Opening inventory |

800 |

6,300 |

Finished goods a/c |

2.800 |

36,400 |

|

Process 1 a/c |

3,000 |

18,100 |

|||

|

Added materials |

9,600 |

||||

|

Conversion costs |

11,800 |

Closing inventory a/c |

1,000 |

9,400 |

|

|

3,800 |

45,800 |

3,800 |

45,800 |

8. Bài tập luyện tập

1. Shiny Co has two processes, Y and Z. There is an expected loss of 5% of input in process Y and 7% of input in process Z. Activity during a four week period is as follows.

Material input: Y: 20,000kg, Z: 28,000kg

Output Y: 18,500kg, Z: 26,100kg

Is there an abnormal gain or abnormal loss for each process?

A. Y: Abnormal loss, Z: Abnormal loss

B. Y: Abnormal gain, Z: Abnormal loss

C. Y: Abnormal loss, Z: Abnormal gain

D. Y: Abnormal gain, Z: Abnormal gain

Answer: C

2. Charlton Ltd manufactures a product in a single process operation. Normal loss is 10% of input. Loss occurs at the end of the process. Data for June areas follows.

|

Opening and closing stocks of working progress |

Nil |

|

Cost of input labor materials (3,300 units) |

$59,100 |

|

Direct labor and production overhead |

$30,000 |

|

Output to finished goods |

2,750 units |

The full cost of finished output in June was

A. $74,250

B. $81,000

C. $82,500

D. $89,100

Answer: C

3. Ashley Co operates a process costing system. The following details are available for Process 2.

Materials input at beginning of process 12,000 kg, costing $18,000. Labor and overheads added $28,000.

10,000 kg were completed and transferred to the Finished Goods account. The remaining units were 60% complete with regard to labor and overheads. There were no losses in the period.

What is the value of Closing WIP in the process account?

A. $4,800

B. $6,000

C. $7,667

D. $8,000

Answer: B

4. Walter Couses the FIFO method of process costing. At the end of a four week period, the following information was available for process P.

Opening WIP 2,000 units (60% complete) costing $3,000 to date

Closing WIP 1,500 units (40% complete)

Transferred to next process 7,000 units

How many units were started and completed during the period?

A. 5,000 units

B. 7,000 units

C. 8,400 units

D. 9,000 units

Answer: A

5. Cheryl Co operates a FIFO process costing system. The following information is available for last month.

Opening work in progress 2,000 units valued at $3,000

Input 60,000 units costing $30,000

Conversion costs $20,000

Units transferred to next process 52,000 units

Closing work in progress 10,000 units

Opening work in progress was 100% complete with regard to input materials and 70% complete as to conversion. Closing work in progress was complete with regard to input materials and 80% complete as to conversion.

What was the number of equivalent units with regard to conversion costs?

A. 44,000

B. 50.600

C. 52,000

D. 58,600

Answer: D

Author: Ngoc Han

Reviewed by: Duy Anh Nguyen