-1.png?height=120&name=SAPP%20logo%20m%E1%BB%9Bi-01%20(1)-1.png)

Như đã nói ở bài 8, chúng ta có 2 phương pháp tính toán chi phí sản xuất phổ biến đó là Phương pháp tính chi phí biên (marginal costing) và Phương pháp phân bổ chi phí (absorption costing). Ở bài trước chúng ta đã tìm hiểu về Absorption costing, tới bài này chúng ta sẽ tìm hiểu về Marginal costing. Từ đó, chúng ta sẽ tìm xem sự khác biệt của 2 phương pháp này ảnh hưởng tới giá trị chi phí sản xuất và giá trị hàng tồn kho như thế nào.

1. Một số định nghĩa

1.1. Marginal cost và marginal costing

Trước hết, chúng ta có marginal cost là chi phí cận biên còn marginal costing là phương pháp tính chi phí cận biên đó.

Nếu đã học môn Kinh tế Vi mô thì hẳn là bạn đã bắt gặp khái niệm này rồi. Về định nghĩa, marginal cost là phần chi phí biến đổi (variable cost) tính trên một đơn vị sản phẩm hay dịch vụ (1 unit of product or service). Điều này nghĩa là cứ tăng thêm 1 đơn vị sản phẩm/ dịch vụ thì tổng chi phí sẽ tăng thêm 1 đơn vị chi phí chính bằng marginal cost.

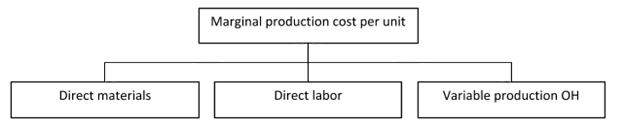

1.2. Marginal production cost per unit

Chi phí sản xuất cận biên tính trên 1 đơn vị sản phẩm bao gồm 3 thành phần chi phí: CP NVL trực tiếp, CP NC trực tiếp và CP overheads biến đổi. Bởi cứ tăng thêm 1 đơn vị đầu ra thì sẽ tăng thêm 1 đơn vị chi phí bao gồm 3 thành phần trên.

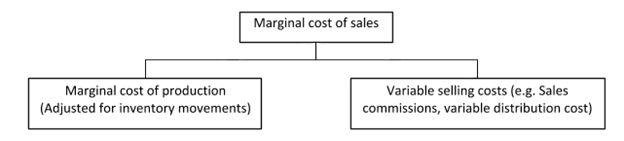

1.3. Marginal cost of sales

Giá vốn hàng bán cận biên sẽ bao gồm 2 bộ phận chi phí là: chi phí sản xuất ra sản phẩm đó và chi phí (biến đổi) để bán sản phẩm đó.

1.4. Contribution margin

Số dư đảm phí hay lãi trên biến phí là phần chi phí chênh lệch giữa giá bán (doanh thu) với chi phí biến đổi. Số dư đảm phí có thể được xác định cho mỗi đơn vị sản phẩm, từng mặt hàng (per unit) hay tính trên tổng số hàng hóa tiêu thụ.

Contribution = Sales - Variable cost of sales

Contribution margin (per unit) = Selling price (per unit) - Marginal cost (per unit)

2. Nguyên tắc trong tính chi phí biên: 4 nguyên tắc

|

Nguyên tắc |

Nội dung |

|

1 |

Những chi phí cố định phát sinh trong kì là không đổi dù cho sản lượng sản đầu ra trong kì có tăng lên còn chi phí biến đổi thì tăng theo sản lượng, vì vậy: a. Doanh thu tăng theo giá trị sản lượng tiêu thụ b. Chi phí tăng theo phần chi phí biến đổi trên từng đơn vị sản phẩm tiêu thụ c. Lợi nhuận tăng theo phần số dư đảm phí trên từng sản phẩm tiêu thụ |

|

2 |

Tương tự như trên, khi Doanh thu giảm theo giá trị từng đơn vị sản phẩm thì lợi nhuận cũng giảm tương ứng với phần số dư đảm phí tính trên đơn vị sản phẩm đó. |

|

3 |

Lợi nhuận được xác định dựa trên Tổng số dư đảm phí. |

|

4 |

Giá trị hàng tồn kho cuối kì được xác định dựa trên phần Chi phí sản xuất biến đổi. |

Ví dụ minh họa:

Rain Until September Co makes a product, the Splash, which has a variable production cost of $6 per unit and a sales price of $10 per unit. At the beginning of September 20X0, there were no opening inventories, and production during the month was 20,000 units. The fixed costs for the month were $45,000 (production, administration, sales, and distribution). There were no variable marketing costs.

Required: Calculate the contribution and profit for September 20X0, using marginal costing principles, if sales were as follows.

(a) 10,000 Splashes

(b) 15,000 Splashes

(c) 20,000 Splashes

Answer:

- Bước 1: Xác định giá trị hàng tồn kho cuối kì theo Marginal production cost ($6 per unit).

- Bước 2: Xác định Profit = Total contribution – Fixed costs.

- Bước 3: Xác định Variable cost of sales và Contribution.

Các bước tính toán được thể hiện trong bảng dưới đây:

|

|

10,000 Splashes |

15,000 Splashes |

20,000 Splashes |

|||

|

$ |

$ |

$ |

$ |

$ |

$ |

|

|

Sales (at $10) |

100,000 |

150,000 |

200,000 |

|||

|

Opening inventory |

0 |

0 |

0 |

|||

|

Variable production cost ($6*20,000) |

120,000 |

120,000 |

120,000 |

|||

|

Less: Value of closing inventory (at marginal cost) |

60,000 ($6*10,000) |

30,000 ($6*5,000) |

_ |

|||

|

Variable cost of sales |

60,000 |

90,000 |

120,000 |

|||

|

Contribution |

40,000 |

60,000 |

80,000 |

|||

|

Less fixed costs |

45,000 |

45,000 |

45,000 |

|||

|

Profit (loss) |

5,000 |

15,000 |

35,000 |

|||

|

Profit (loss) per unit |

$0.5 |

$1 |

$1.75 |

|||

|

Contribution per unit |

$4 |

$4 |

$4 |

|||

3. So sánh Marginal costing với Absorption costing và đối chiếu lợi nhuận

a. So sánh Marginal Costing và Absorption Costing

|

Marginal costing (MC) |

Absorption costing (AC) |

|

Cung cấp thông tin quản trị hỗ trợ việc dự toán và đưa ra quyết định. |

Thường dùng trong việc xác định lợi nhuận. Dùng cho mục đích kế toán tài chính. |

|

Giá trị HTK cuối kì tính theo Marginal production cost (chỉ tính phần chi phí biến đổi variable cost). |

Giá trị HTK cuối kì bao gồm đầy đủ các chi phí (định phí và biến phí) phát sinh trong quá trình sản xuất (full production cost). |

|

Chi phí cố định ghi nhận vào chi phí trong kì (fixed costs are period costs). |

Chi phí cố định được tính vào giá thành sản phẩm (fixed costs are absorbed into unit costs). |

|

Fixed overheads không được bao gồm trong COS. |

Fixed overheads được bao gồm trong COS. |

Từ đây có thể rút ra kết luận:

Giá trị HTK tính theo MC < Giá trị HTK tính theo AC

Ví dụ minh họa:

The overhead absorption rate for product X is $10 per machine hour. Each unit of product X requires five machine hours. Inventory of product X on 1.1.X1 was 150 units and on 31.12.X1 it was 100 units.

What is the difference in profit between results reported using absorption costing and results reported using marginal costing?

A. The absorption costing profit would be $2,500 less

B. The absorption costing profit would be $2,500 greater

C. The absorption costing profit would be $5,000 less

D. Absorption costing profit would be $5,000 greater

Answer: A

Difference in profit = change in inventory levels.

Fixed overhead absorption per unit: (150 –100) x $10 x 5 = $2,500

Lợi nhuận sẽ giảm do inventory levels giảm. Điểm mấu chốt ở đây là sự thay đổi của sản lượng HTK. Inventory levels giảm dẫn tới việc sử dụng AC sẽ tạo ra ít lợi nhuận hơn. Do đó, loại đáp án B và D.

Lựa chọn C là không chính xác bởi vì chỉ mới tính đến giá trị hàng tồn kho cuối kì (100 units x $10 x 5 hours).

b. Đối chiếu lợi nhuận (profit reconciliation)

Phương pháp đối chiếu sẽ giúp xác định sự chênh lệch trong lợi nhuận giữa 2 phương pháp tính chi phí.

Difference in profits = Change in inventory levels ⨯ overhead absorption rate.

Những kết quả đối chiếu sẽ cho ta kết luận tương ứng:

|

Increase in inventory in a period |

Decrease in inventory in a period |

|

Opening inventory < Closing inventory |

Opening inventory > Closing inventory |

|

Profit: AC > MC |

Profit: AC < MC |

Ví dụ minh họa:

Last month a manufacturing company's profit was $2,000, calculated using absorption costing principles. If marginal costing principles has been used, a loss of $3,000 would have occurred. The company's fixed production cost is $2 per unit. Sales last month were 10,000 units.

What was last month's production (in units)?

A. 7,500

B. 9,500

C. 10,500

D. 12,500

Answer: D

Any difference between marginal and absorption costing profit is due to changes in inventory.

|

$ |

|

|

Absorption costing profit |

2,000 |

|

Marginal costing loss |

3,000 |

|

Difference |

5,000 |

MC profit < AC profit suy ra HTK tăng – nghĩa là, production lớn hơn sales 2,500 units.

Production = 10,000 units (sales) + 2,500 units = 12,500 units.

4. Bài tập luyện tập

1. Marginal costing and absorption costing are different techniques for assessing profit in a period. If there are changes in inventory during a period, marginal costing and absorption costing given different results for profit obtained.

Which of the following statements are true?

(I) If inventory levels increase, marginal costing will report the higher profit.

(II) If inventory levels decrease, marginal costing will report the lower profit.

(III) If inventory levels decrease, marginal costing will report the higher profit.

(IV) If the opening and closing inventory volumes are the same, marginal costing and absorption costing will give the same profit figure.

A. All of the above

B. I, II and IV

C. I and IV

D. III and IV

Answer: D

2. Which of the following are arguments in favor of marginal costing?

A. Closing inventory is valued in accordance with IAS 2.

B. It is simple to operate.

C. There is no under or over absorption of overheads.

D. Fixed costs are the same regardless of activity levels.

E. The information from this costing method may be used for decision making.

Answer: B, C, D, E

3. The overhead absorption rate for product T is $4 per machine hour. Each unit of T requires 3 machine hours. Inventories of product T last period were:

Opening inventory 2,400 units

Closing inventory 2,700 units

Compared with the marginal costing profit for the period, the absorption costing profit for product T will be which of the following?

A. $1,200 higher

B. $3,600 higher

C. $1,200 lower

D. $3,600 lower

Answer: B

Author: Ngoc Han

Reviewed by: Duy Anh Nguyen